Read this article in: Deutsch | Español | Français | עברית | Italiano | 日本語

by Jeff Miller, Chief Investment Officer | Download the full report (PDF)

The world is in the midst of what could be an era-defining evolution. The opportunities brought about by AI are incredibly exciting but it is coming at a time of increased fragility across a number of other larger economic forces. We are undergoing a period where every year seems to bring a new set of significant macro and geopolitical events, which creates a challenging backdrop for investors.

These events are occurring with increased frequency and we think this is due to a number of larger structural forces at play, including a changing geopolitical landscape, a seismic technological shift, an increasingly polarized political landscape, and higher amounts of leverage in the system. But through it all, economic growth is holding up and public equity market performance has been strong. We think this dichotomy can be explained by AI-related growth and spend, as well as the amount of monetary and fiscal support that is at play.

Geopolitics and AI driving global uncertainty

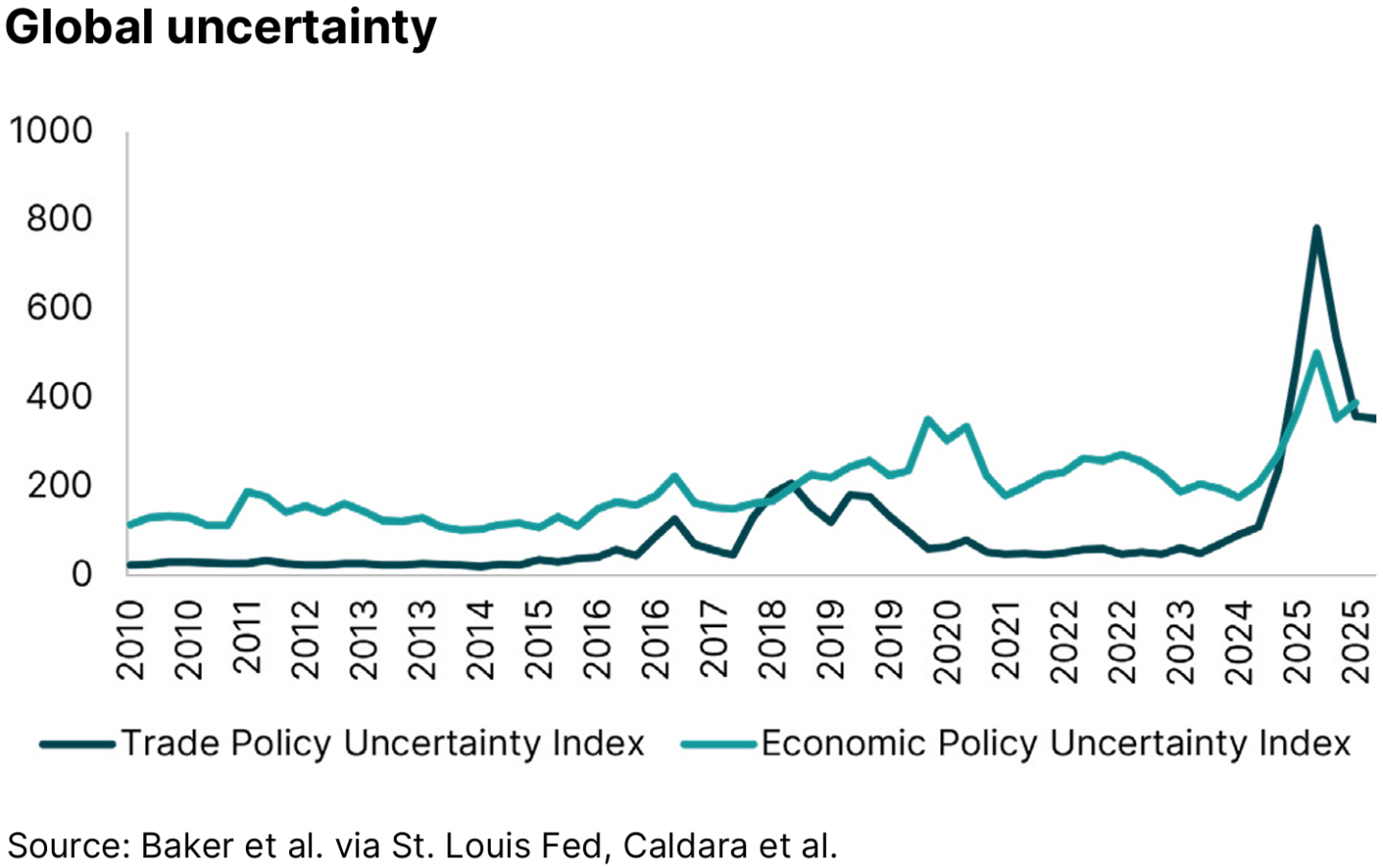

The economic backdrop at the mid-point of 2026 is truly remarkable. There is such a dramatic shift underway in our geopolitics that some have called it the end to the post-World War Two order: it’s showing in trade tensions and tariffs, in two separate military conflicts, and in the supply shocks that have emerged from them. In some areas, politics are as polarized as they’ve ever been, and the growth in government spending and debt is inexorable. In addition, while AI is clearly a significant and exciting opportunity, it also represents a risk to certain industry segments and labor pools. And as long as these larger issues are in play, we should expect a greater level of volatility, higher levels of uncertainty, and dampened consumer confidence.

In the US, consumer confidence has already fallen to its lowest recorded level since the University of Michigan survey began in 1952.

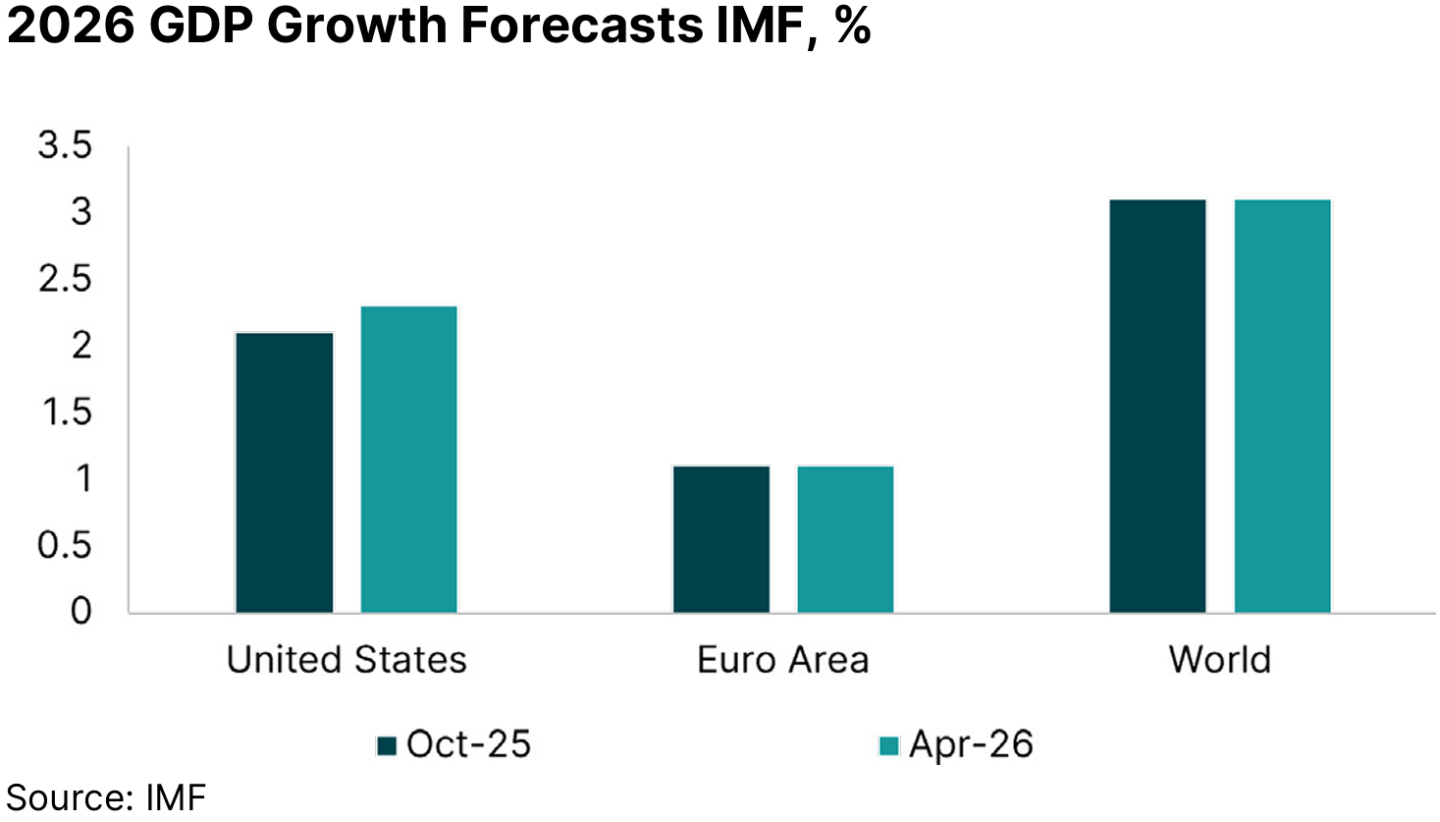

But surprisingly, against this volatile and uncertain backdrop, there’s been real resilience in global growth, and GDP forecasts have remained intact.

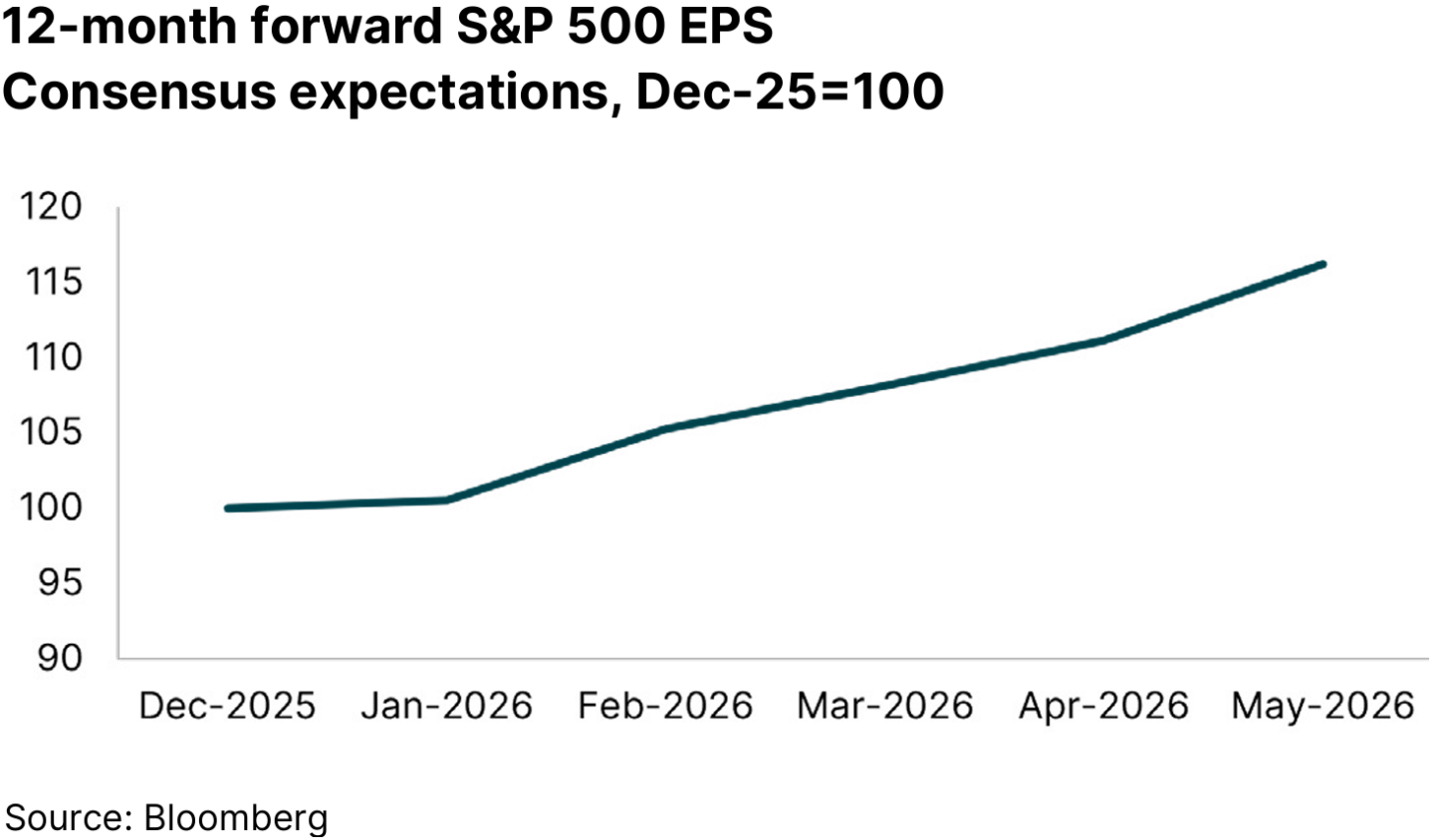

Corporate earnings have also remained strong in theUS, with 12-month forward earnings projections actually accelerating.

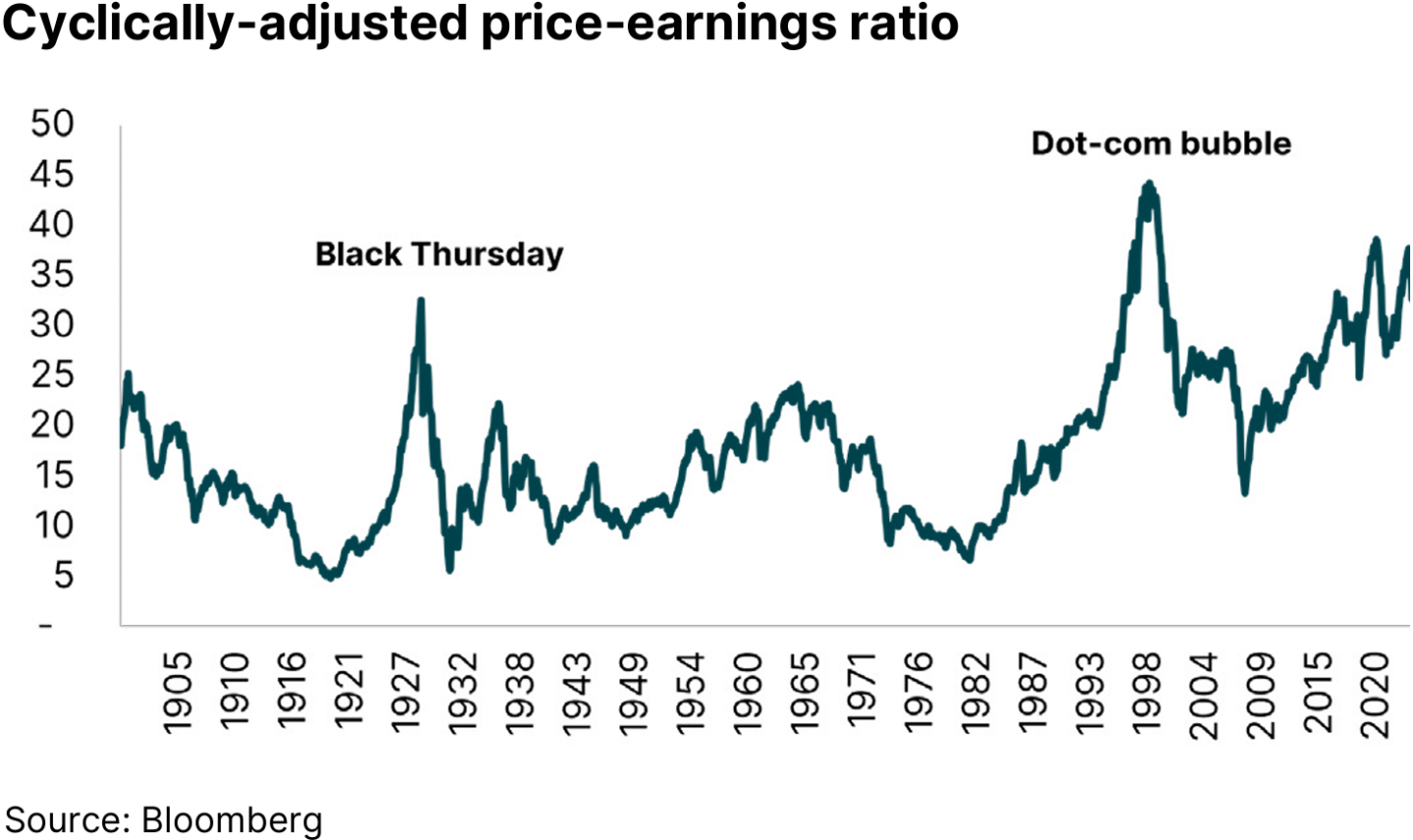

Similarly, the public market performance across many regions has been very strong, no more so than in the S&P 500, where valuations are now close to an all-time high.

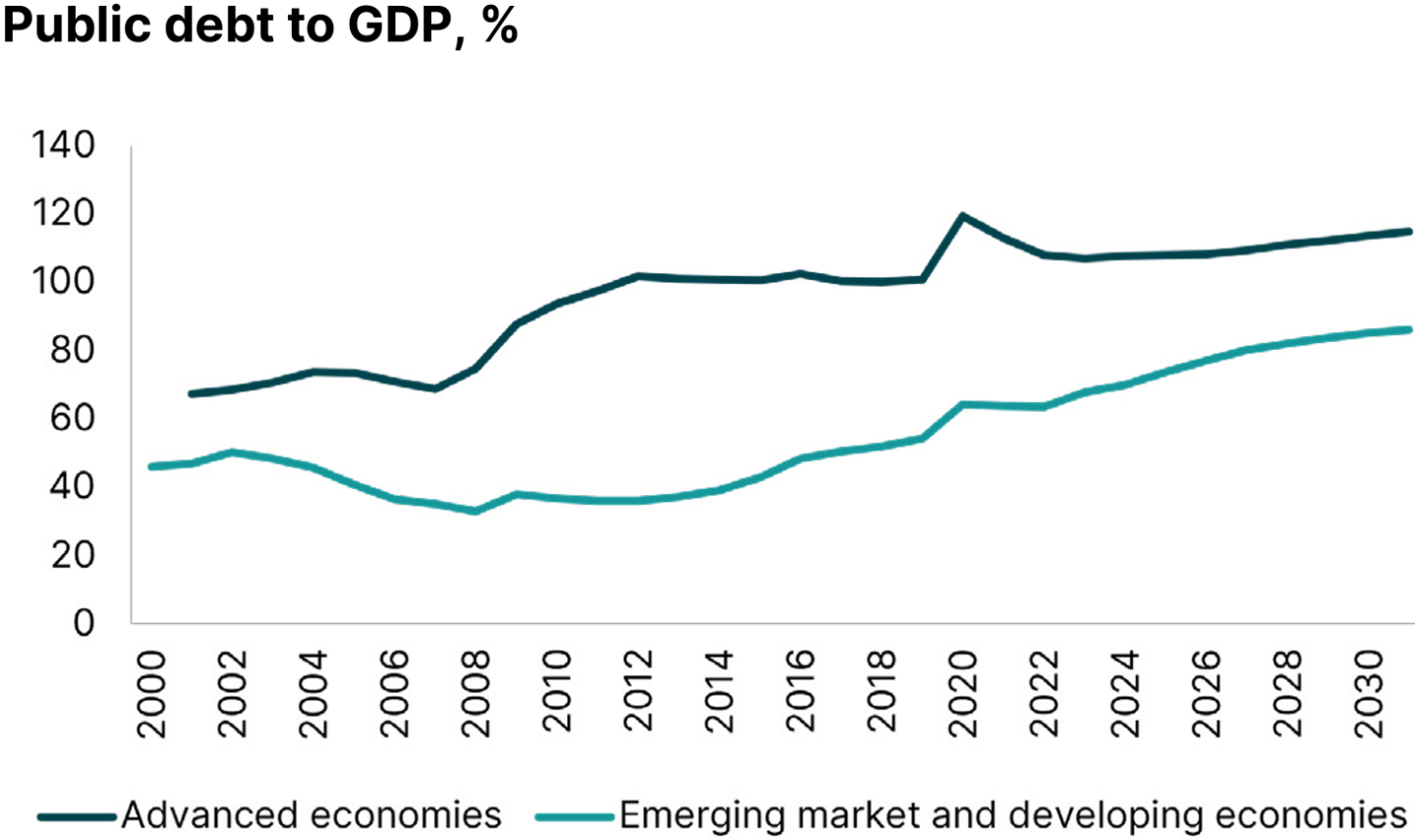

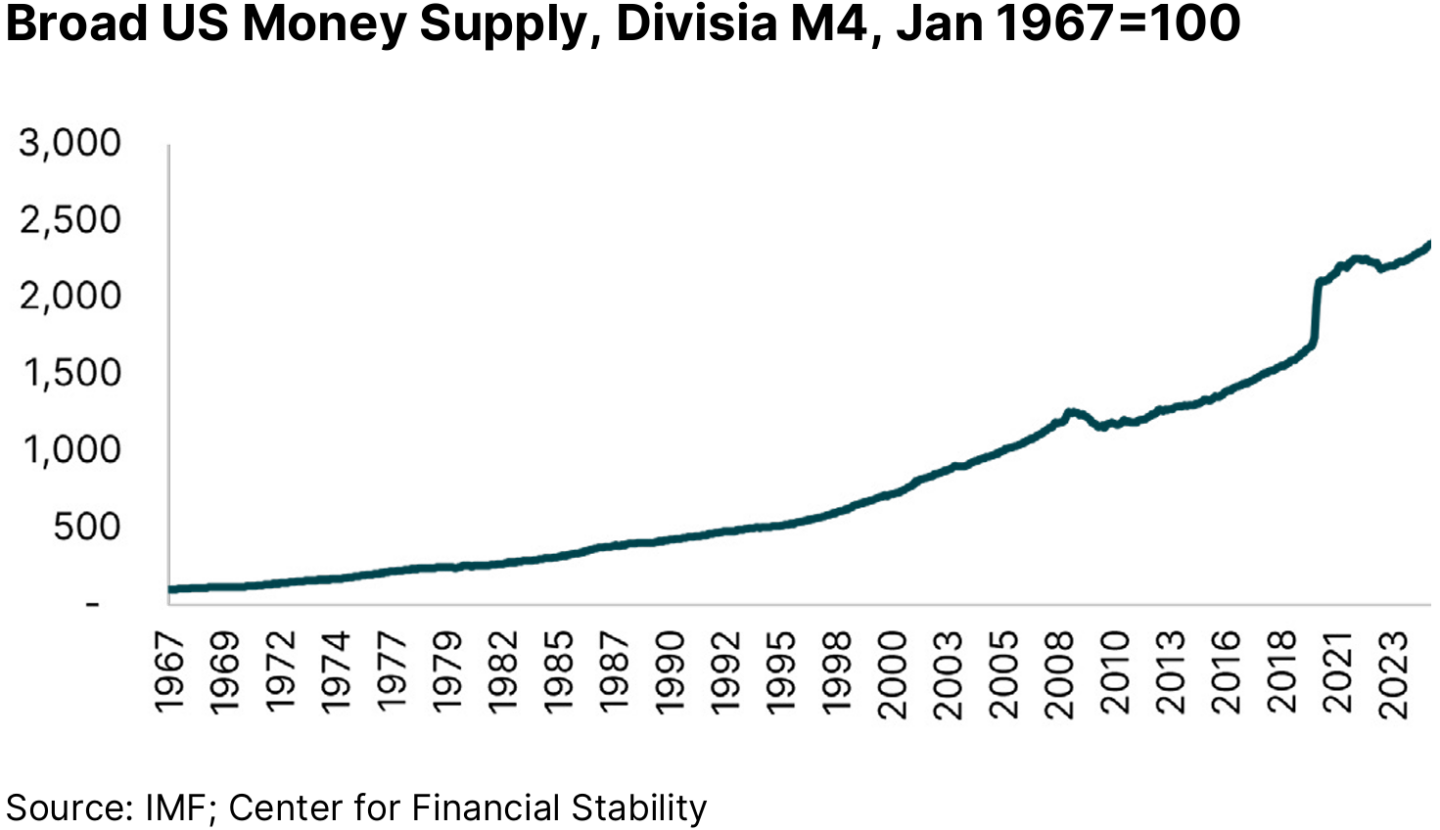

Why, when so many large, transformative events are happening across the world, has there not been more of an impact across our markets and economies? In part, the markets’ resilience has been supported by the significant level of liquidity now at play in the system. Public debt to GDP is now well over 100% for advanced economies, and emerging markets are on their way to these levels.

Many economists believe the elevated level of monetary and fiscal stimulus is finding its way into corporate profits which continue to be high relative to historical levels – a dynamic that simultaneously supports market valuations and makes the inflation problem harder to solve.

The AI risk – and opportunity

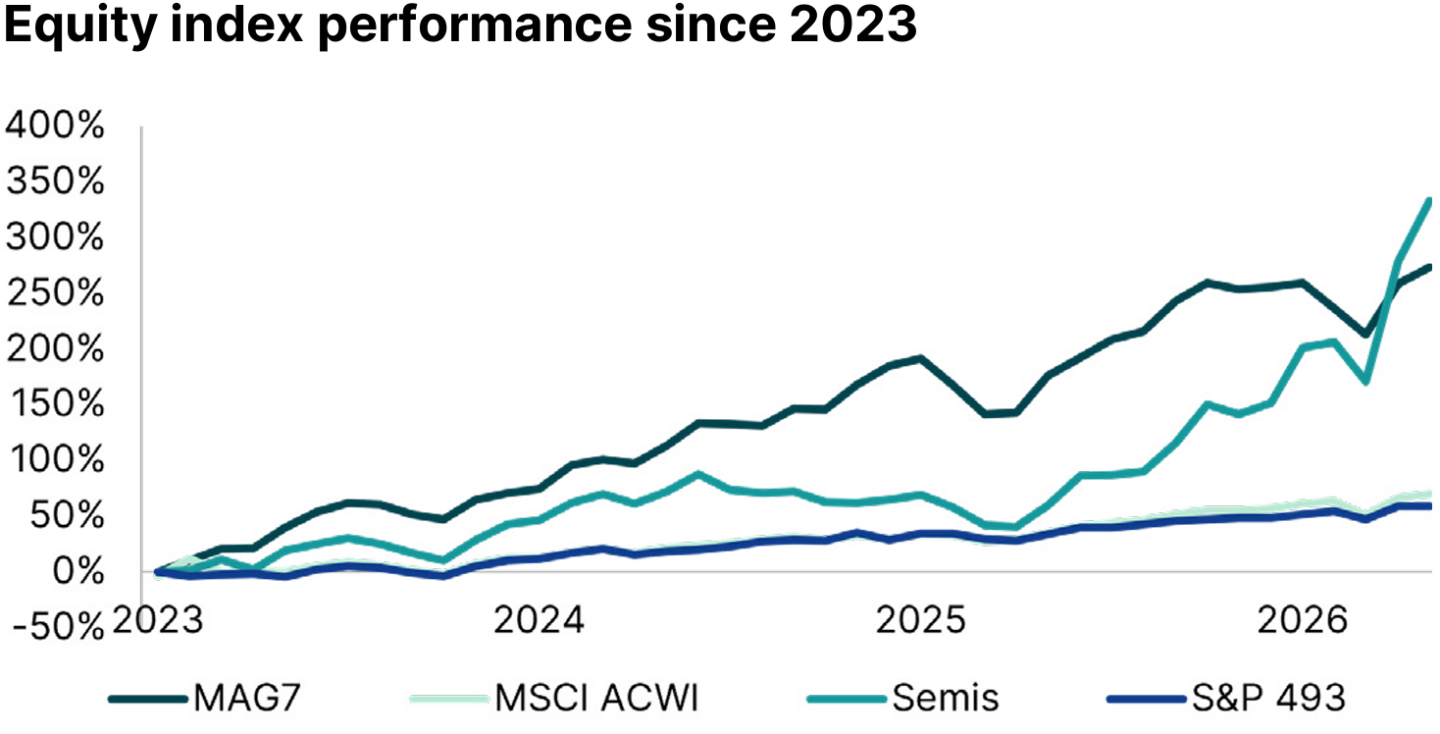

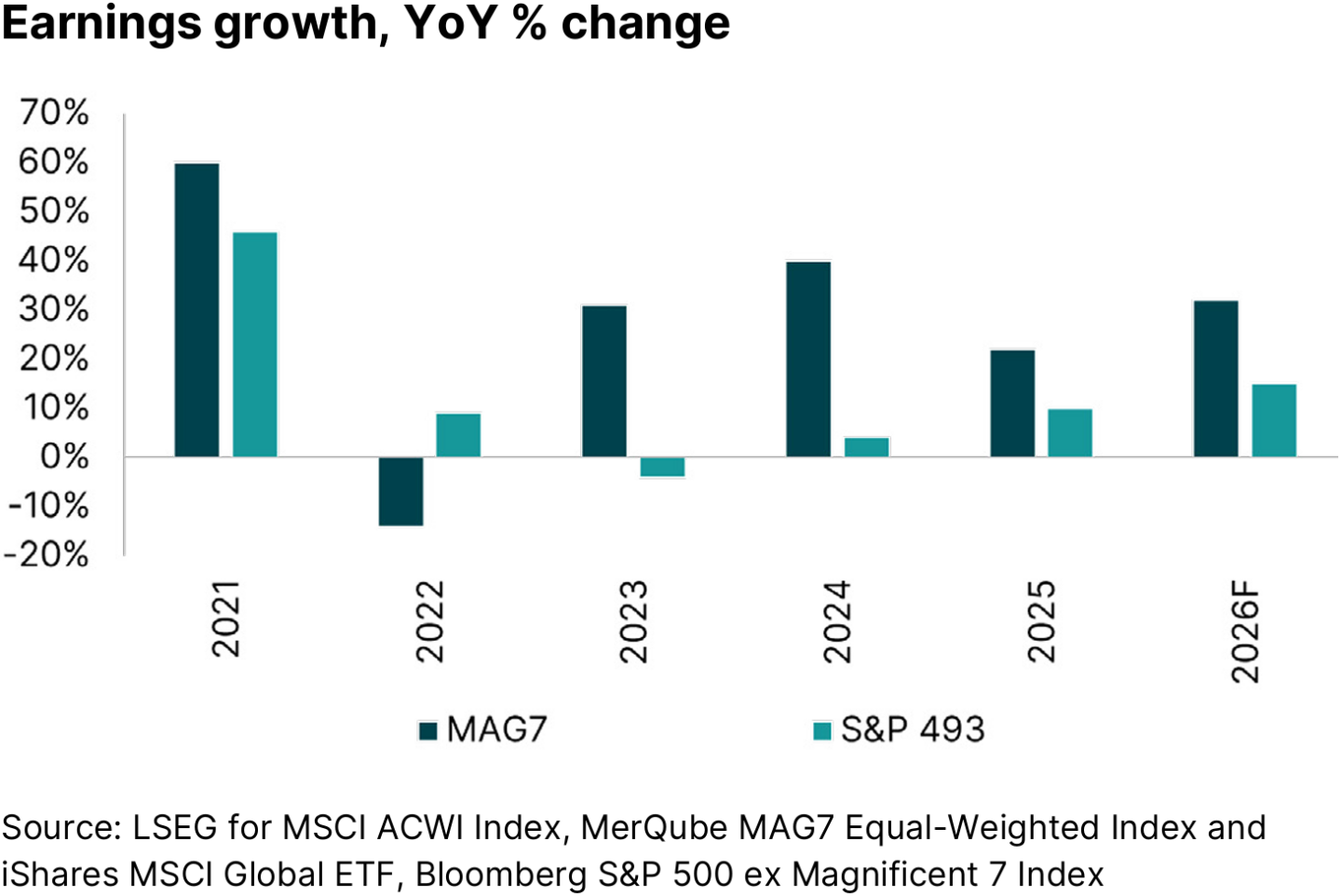

The wider economic resilience though has also been driven by the strength of the AI trade. In particular, in public markets, we’ve seen a strong performance from The Magnificent Seven technology stocks and semiconductor companies really driving the market forward, while the AI productivity boom has helped mitigate any weaker earnings across the rest of the S&P 500.

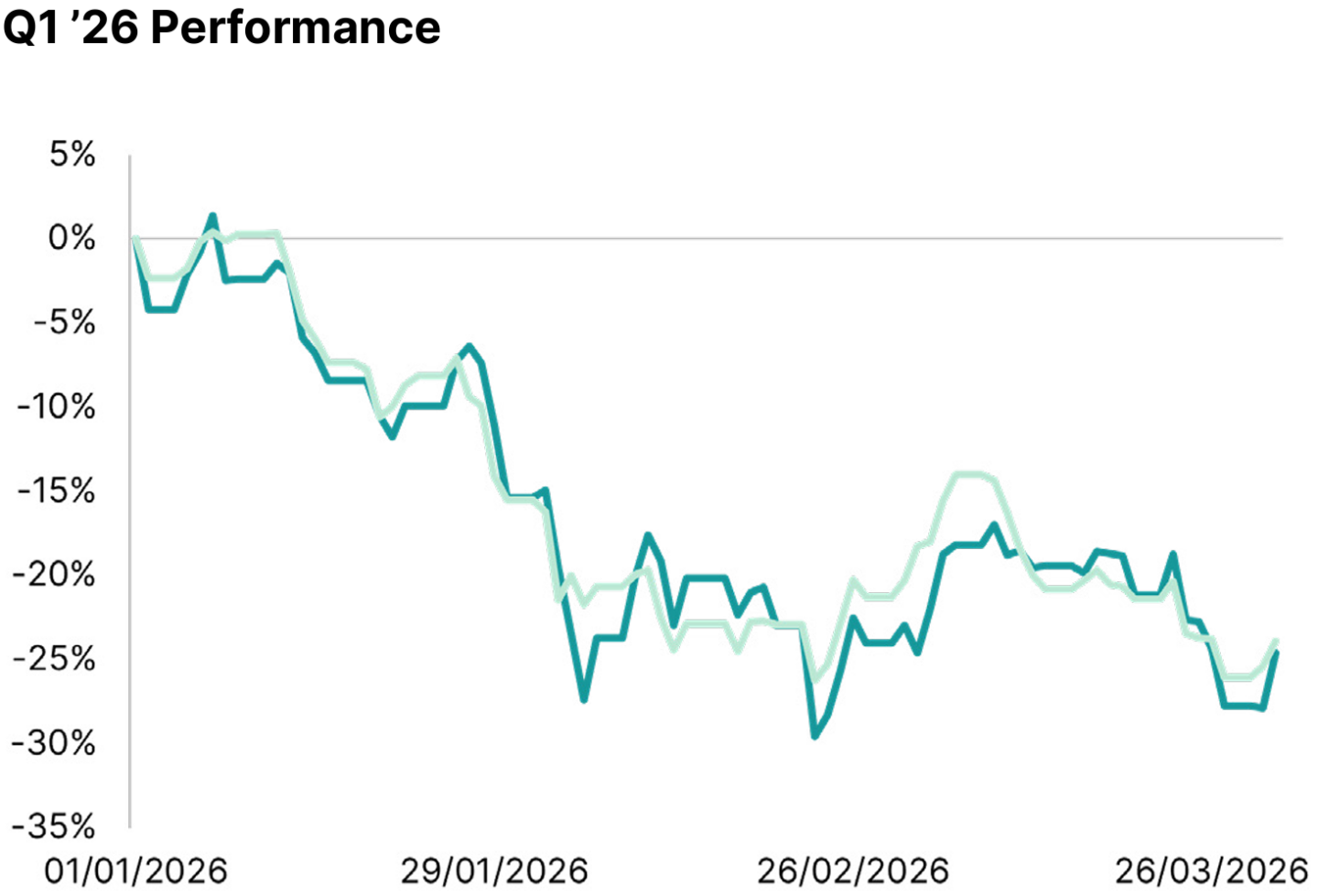

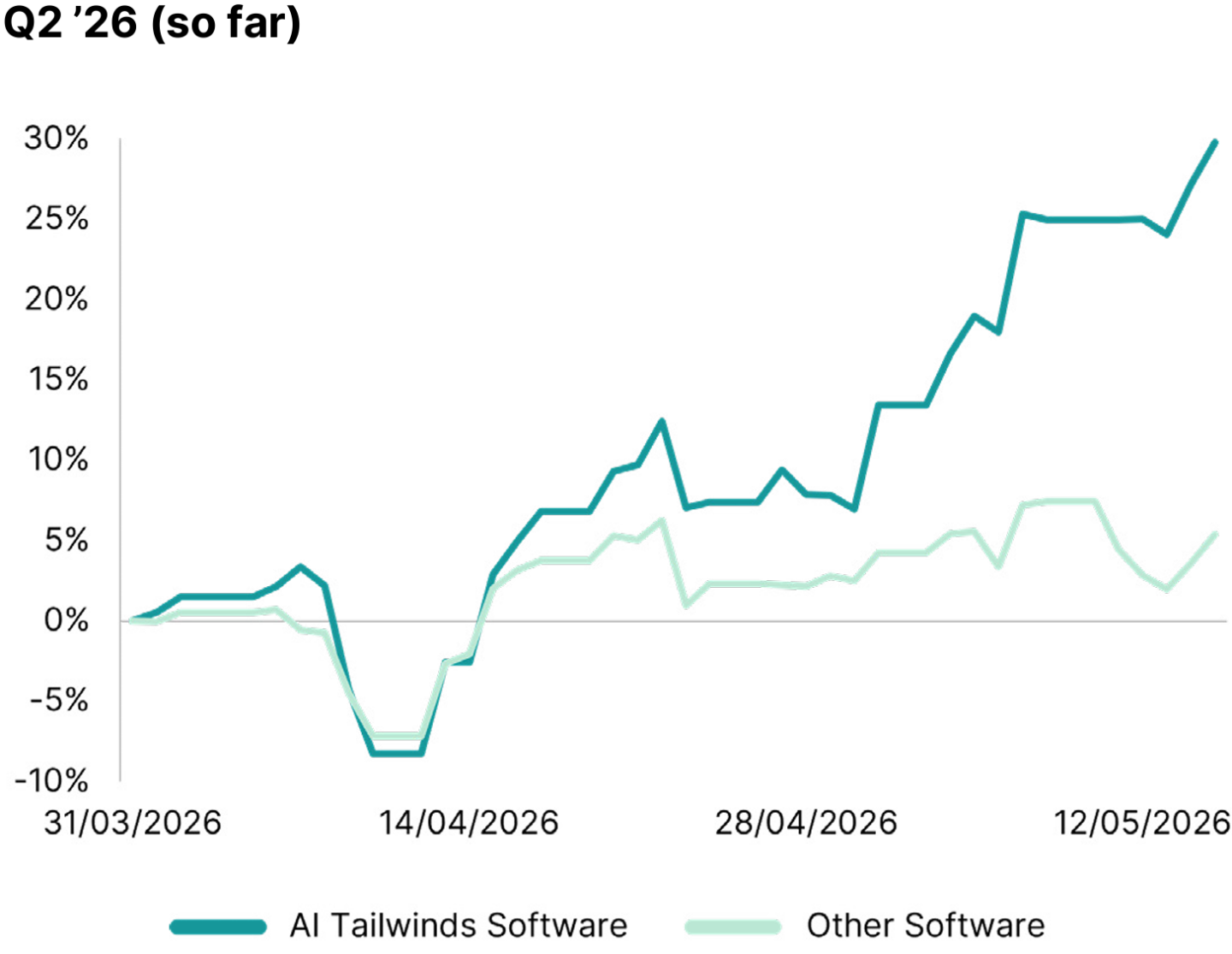

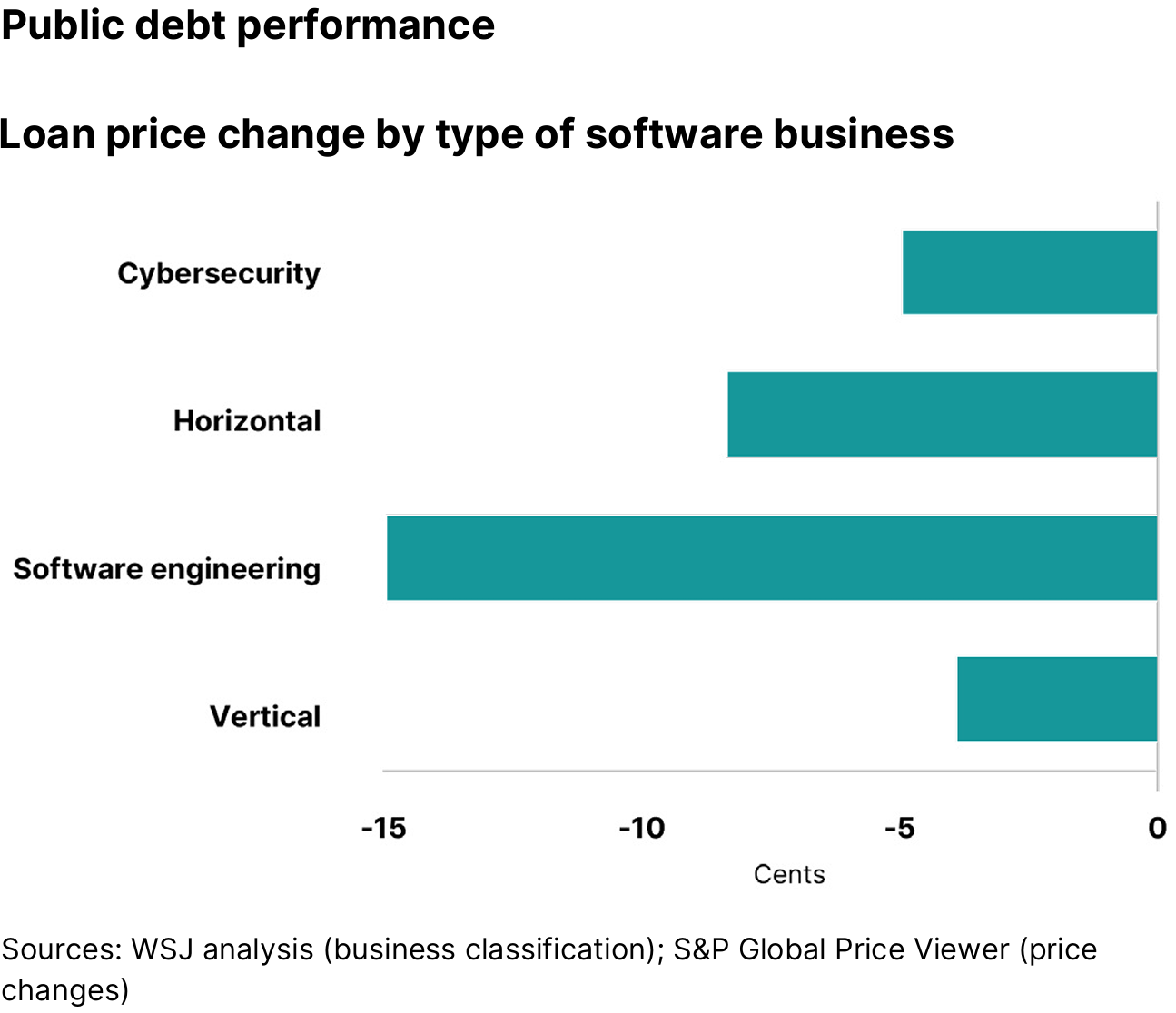

The first half of 2026 brought plenty of doom and gloom headlines around software and AI risk, with the SaaSpocalypse 48-hour sell-off in February wiping around $285 billion from software-as-a-service valuations. But at the end of the first half, it is becoming clear that companies with the right attributes – those that are well embedded with their customer base and with handling their client data – may be set up to win in this environment. These are the firms that may have the opportunity to use AI to deepen their relationships with their customers and to open up new revenue streams within their client bases, and already SaaS companies are buying, developing, and embedding AI tools to develop their capabilities.

There is, however, real pressure on those firms that do not have the best attributes, and this dynamic is creating real dispersion in the market. We’re currently in the midst of that sorting process, dividing the winners from the losers, but what is clear is that while the outcome for software firms is not going to be as bad as was initially feared, the outlook is never going to be as good as it once was for all software.

Whatever happens with software firms, it’s clear there’s a huge opportunity emerging with the AI infrastructure buildout.

The amount spent globally on AI-related infrastructure may reach $2.6 trillion in 20261, and the AI data center build-out is projected to require nearly $7 trillion by 20302.

These figures of course suggest that the size of the opportunity here is incredible. But it’s worth remembering that many big technological shifts we’ve seen in the past have been accompanied at some point in the cycle by overspending, overbuilding, and overvaluation. It was something seen with the development of the UK railroads, the telecommunications correction, and even in the buildup of the internet in the late 1990s and early 2000s – all of these brought significant valuation growth, and then subsequent correction.

With economists noting that current spending on the buildout in AI is already contributing around 1% to US real GDPgrowth3, this is an issue that’s clearly having a huge impact on our economic outlook, and valuations and performance across the public markets.

Private markets stay strong

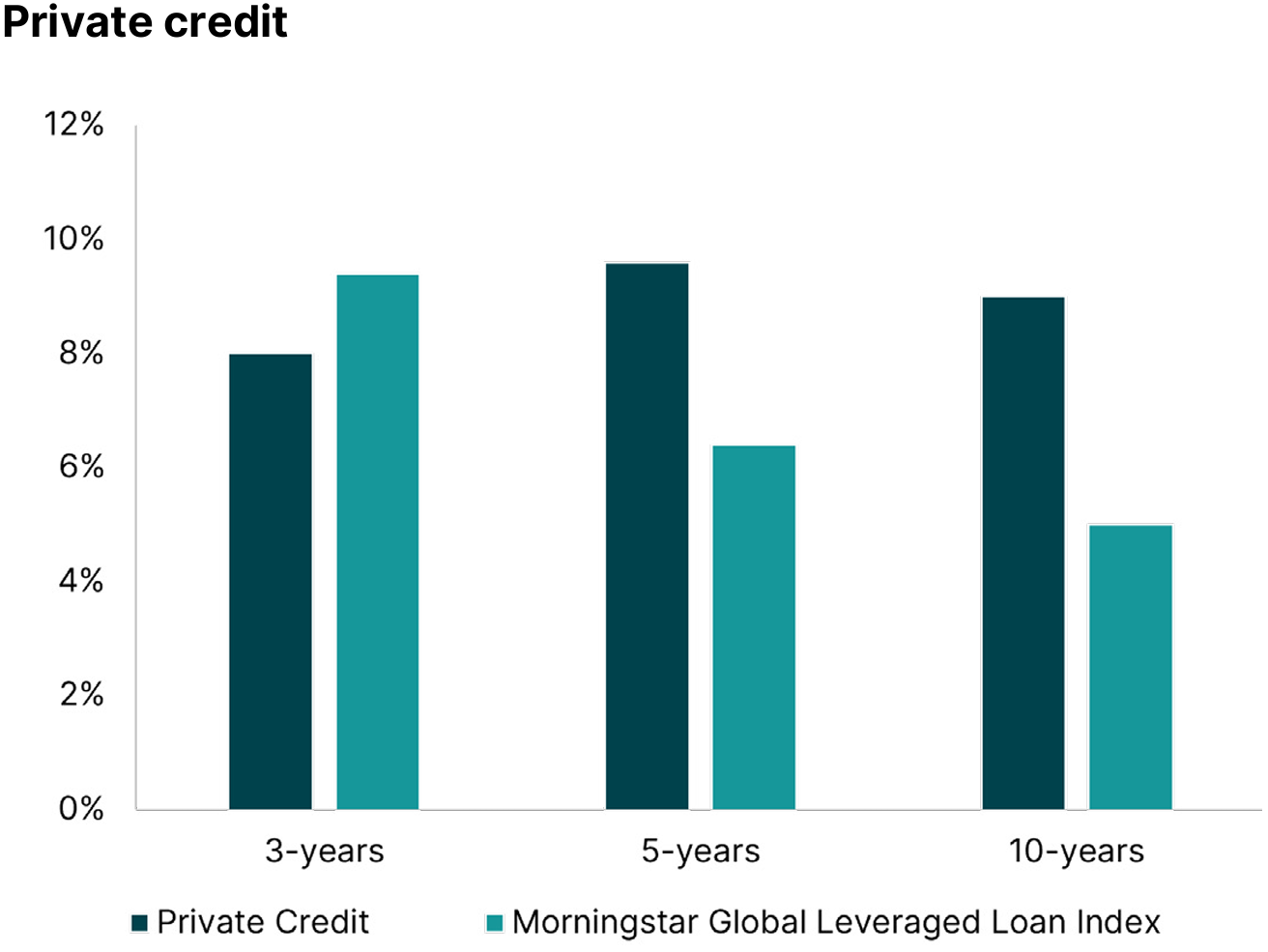

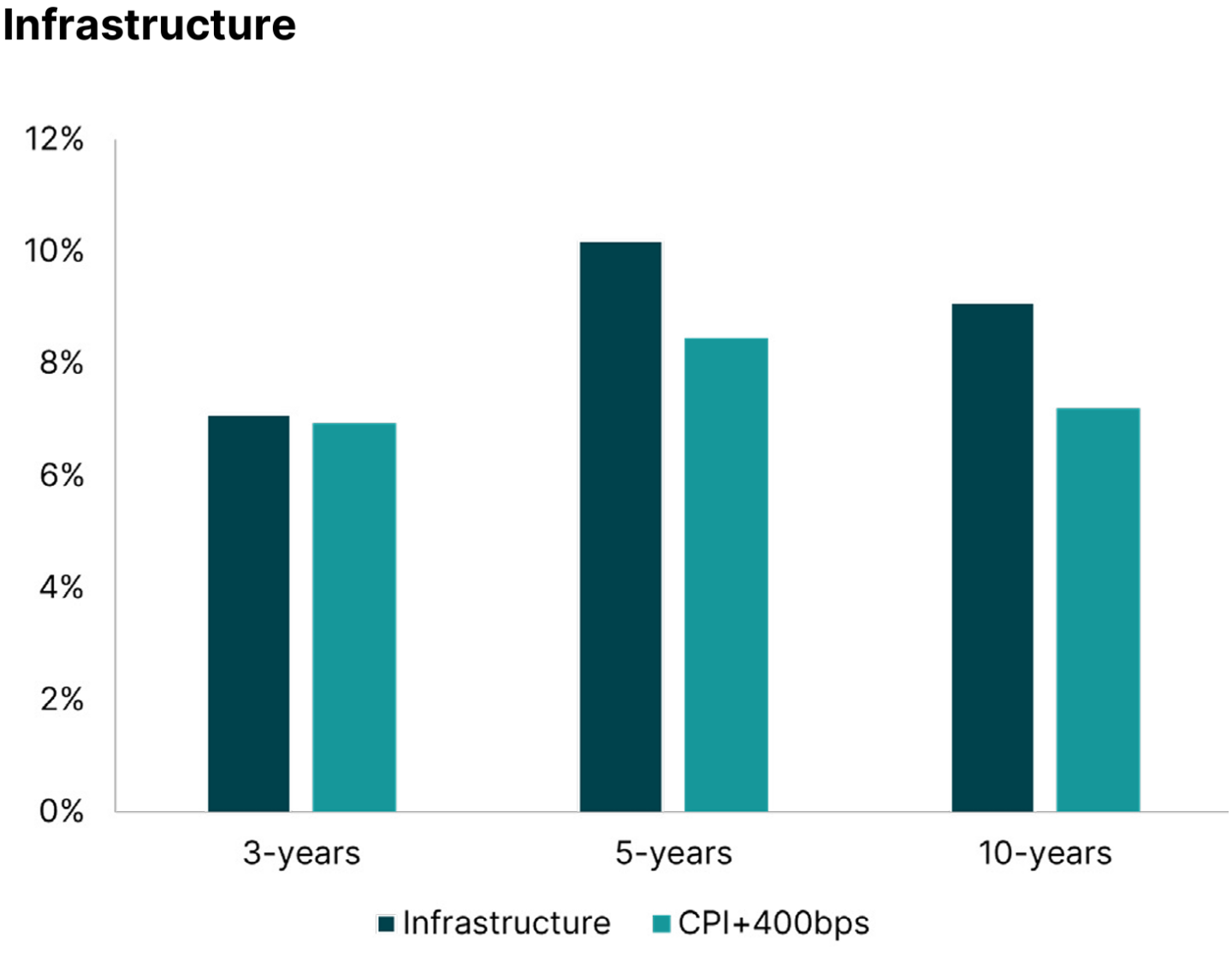

Within the private markets, over the medium and longer term returns remain robust compared to their public counterpart indices, in particular across credit and infrastructure.

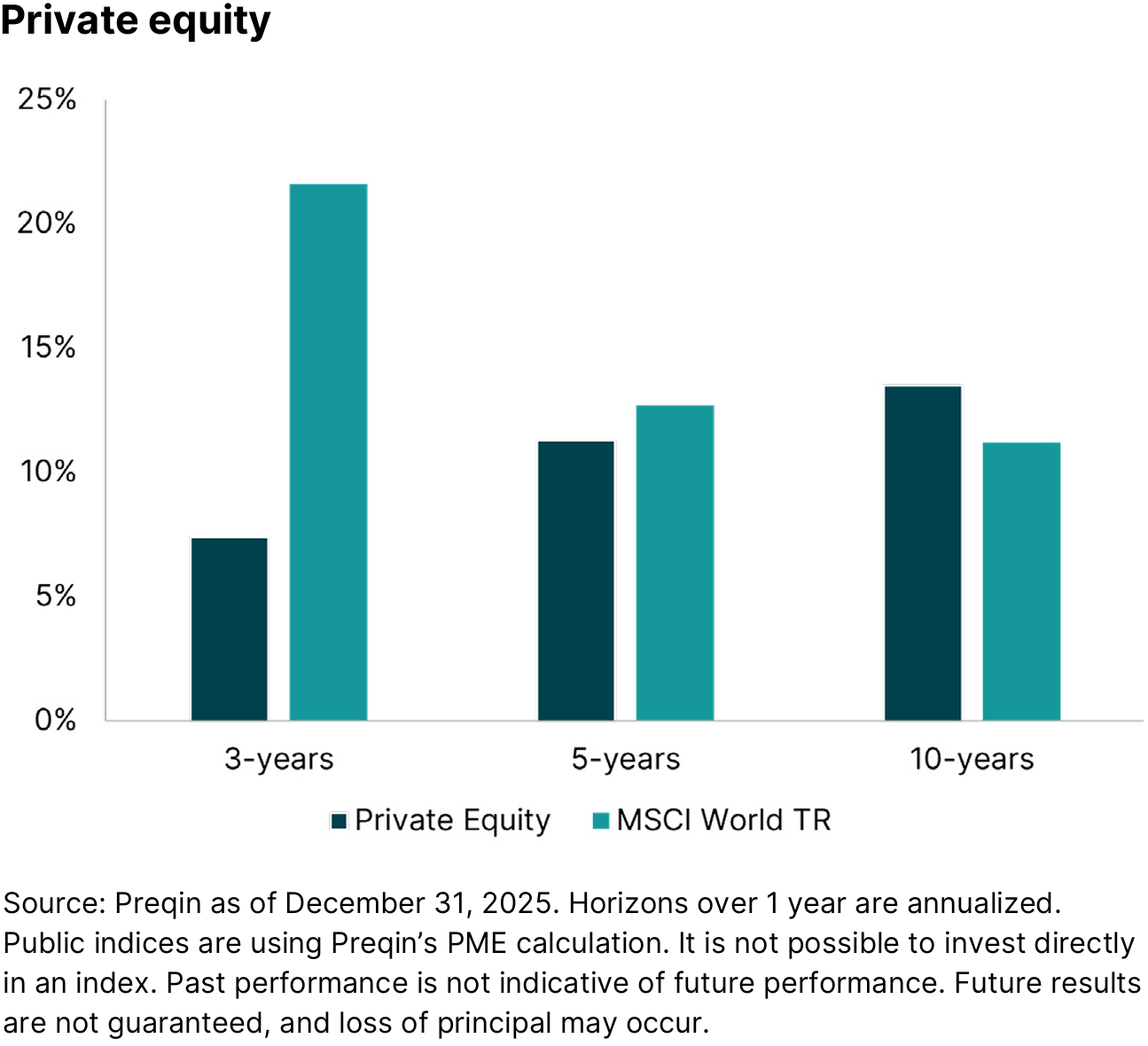

In private equity, the comparables with public markets look tougher, in part due to the strength of the performance of public markets, but also due to more subdued private equity returns of late. This is an issue that has been more acute in the US than in Europe, but the combination of the higher purchase prices and interest rate hikes over the last half decade has resulted in multiple compressions across portfolios and lower exit activity.

Although we’ve seen strong operating performance in our private equity portfolios, this is not translating into growth in portfolio values across the markets. However, the discrepancy in performance between private and public markets should result in some improvement in private equity markets: we’ve already seen some sequential improvements in NAV growth within our portfolios.

Volumes increase

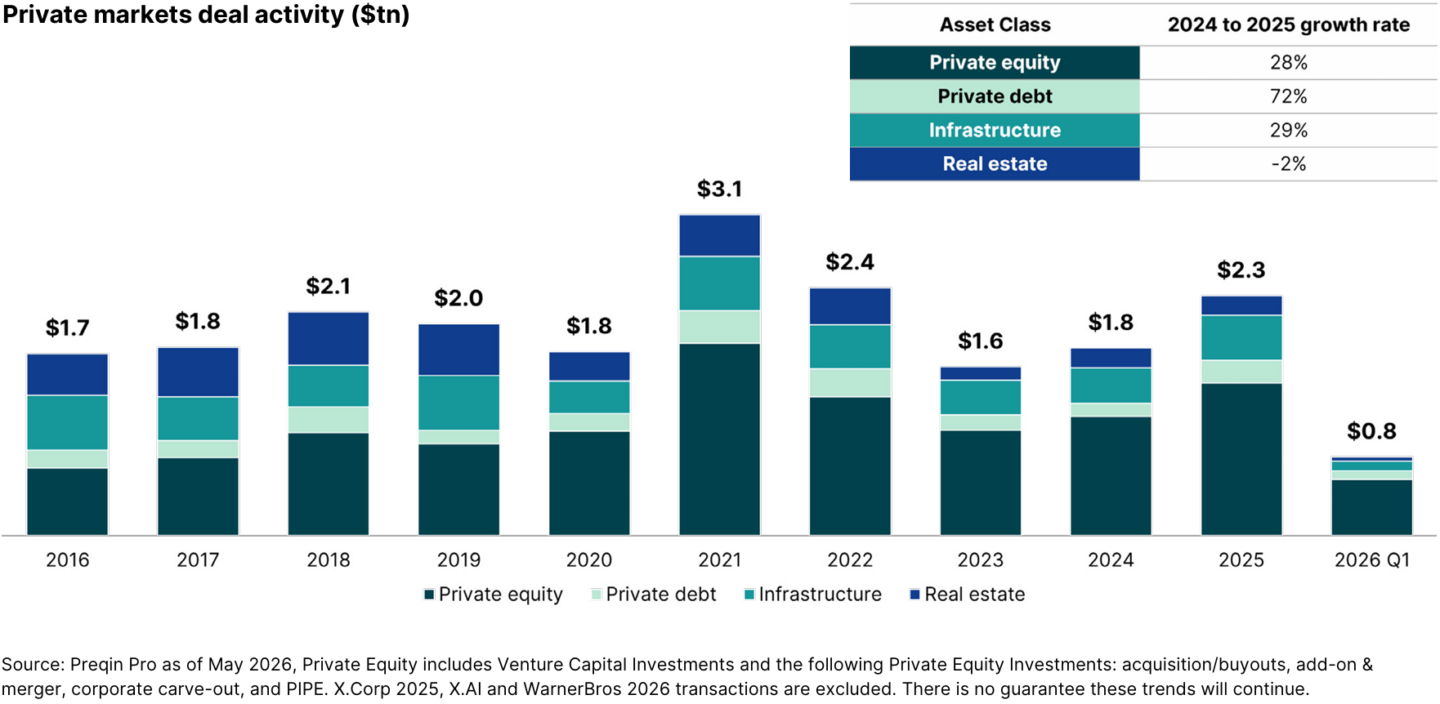

At the end of the first half of 2025, we noted that any clarity around tariffs could result in a pick-up in volumes, and that was exactly what we got. Overall, private market volumes increased around 30% last year, driven by ramping activity in the second half, and 2026 has started strongly.

In 2025, private equity volumes reached the second highest year for deal volume on record, boosted not least by the $57 billion buyout of video games firm Electronic Arts.

In private credit, global volumes rose around 70%, driven by the increase in private equity volumes, a pick-up in refinancing activity, and financings supporting the build-out of AI infrastructure. AI and digital infrastructure demand also supported the 30% growth of infrastructure volumes, alongside the higher growth in renewables and larger deal sizes.

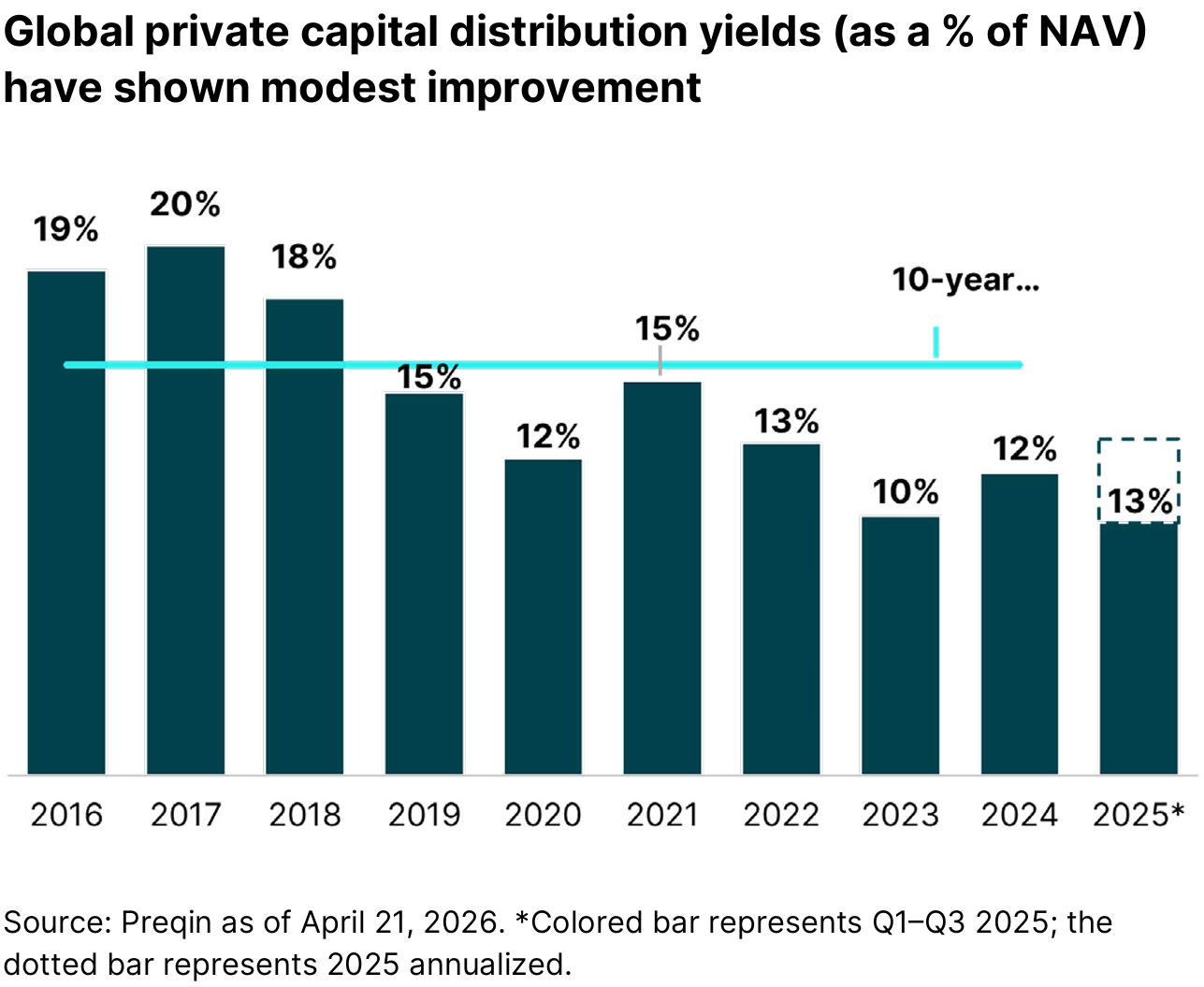

The landscape for exits and distributions continues to improve, albeit modestly, with distribution rates still below historical levels.

Although the 13% distribution rate anticipated for the full year 2025 is up versus 2024, we are still far from the 10-year average of 16%. We never expected a speedy return to a more normalized rate of exits and there continues to be a large backlog of aged companies. The continued sub-par distribution rate is having a dampening effect on fundraising.

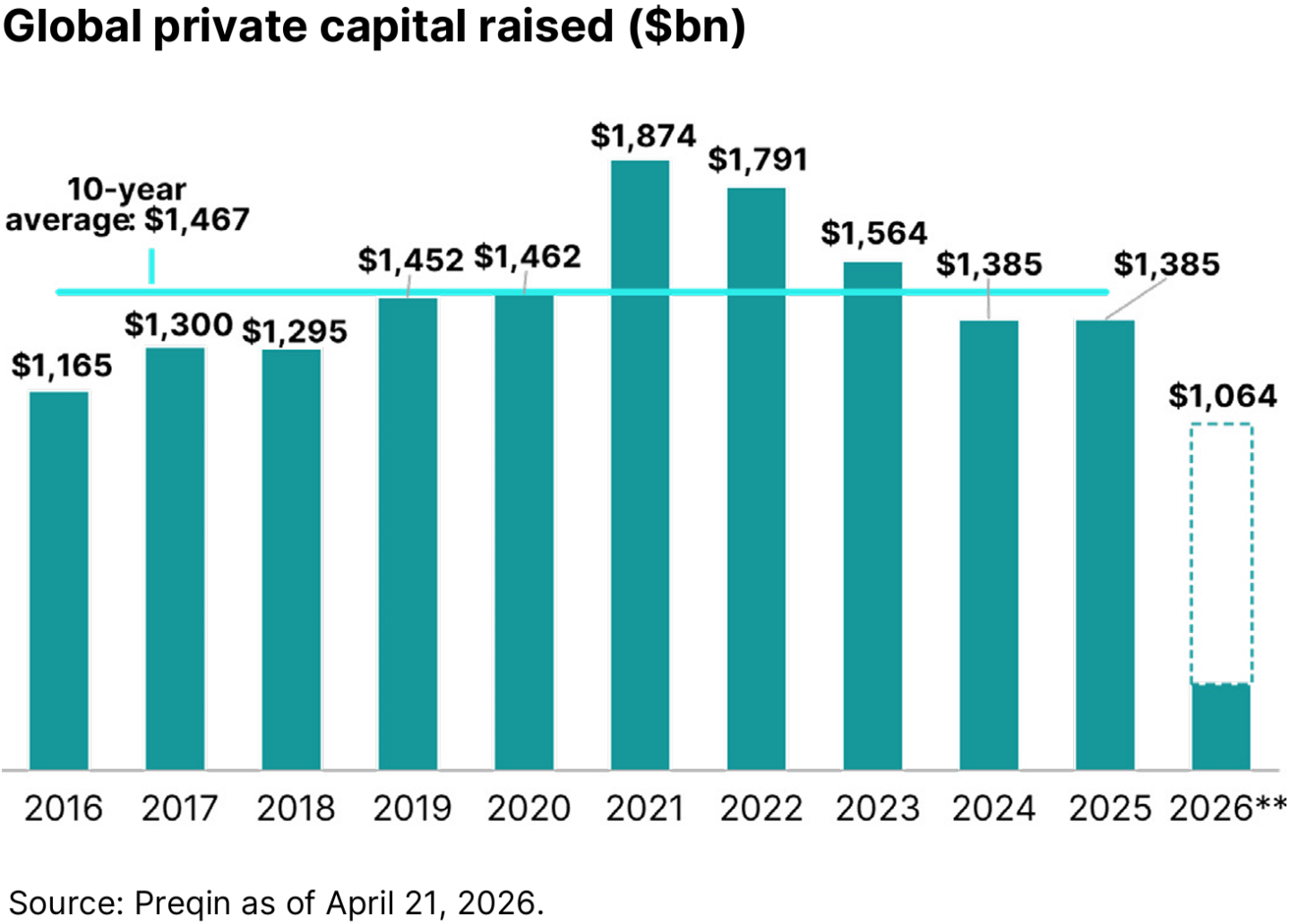

Overall, fundraising in 2025 was flat on the previous year, but infrastructure fundraising was a real standout. Fundraising in this market was up more than 50% from 2024, making it the highest year on record, owing in part to investors moving to the long-term stability of the infrastructure asset class in times of volatility and also due to investors being under-allocated to infrastructure.

While fundraising figures in private equity and private credit were down in 2025, the silver lining here is that we are chipping away at the amount of dry powder available, creating a better balance in the market between the supply of capital and the rate of deal flow.

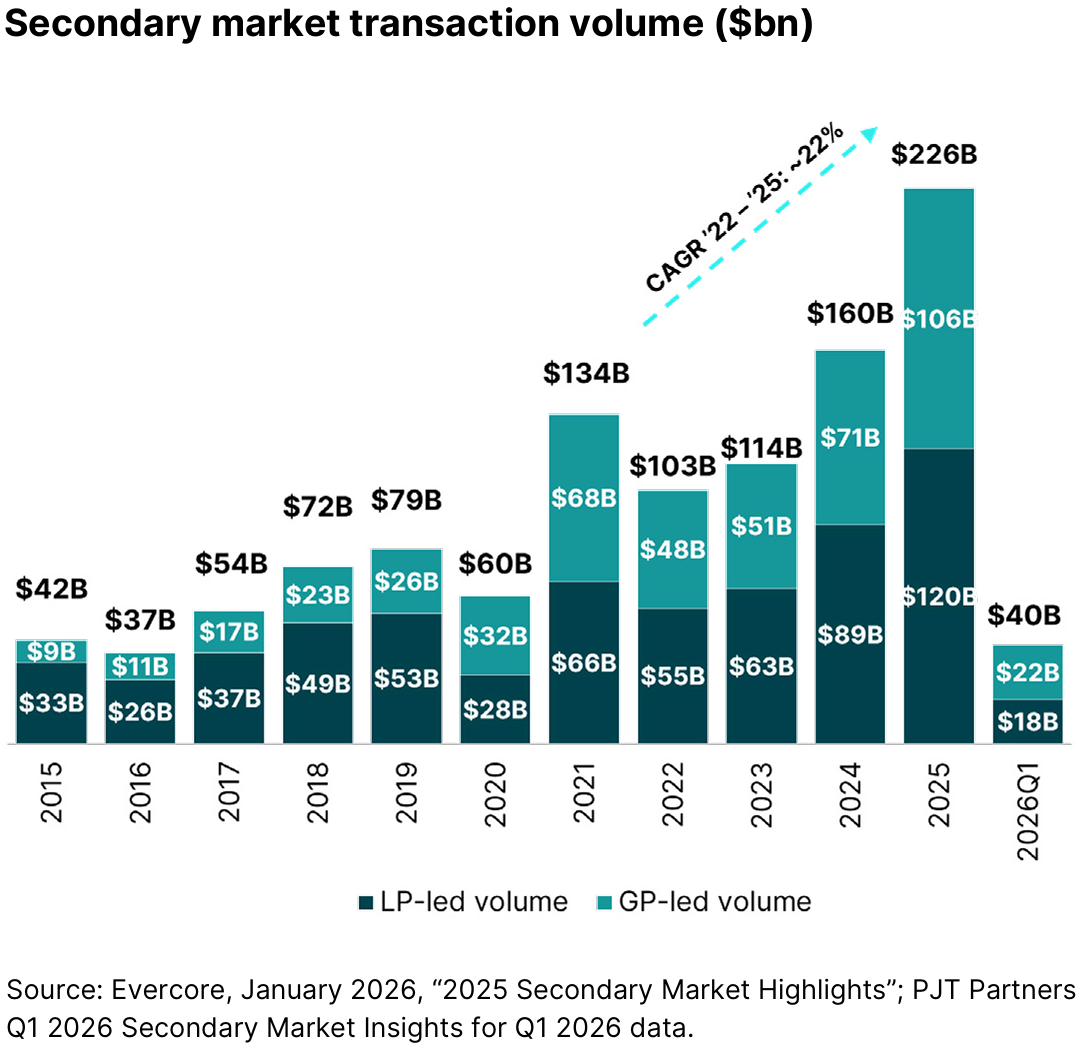

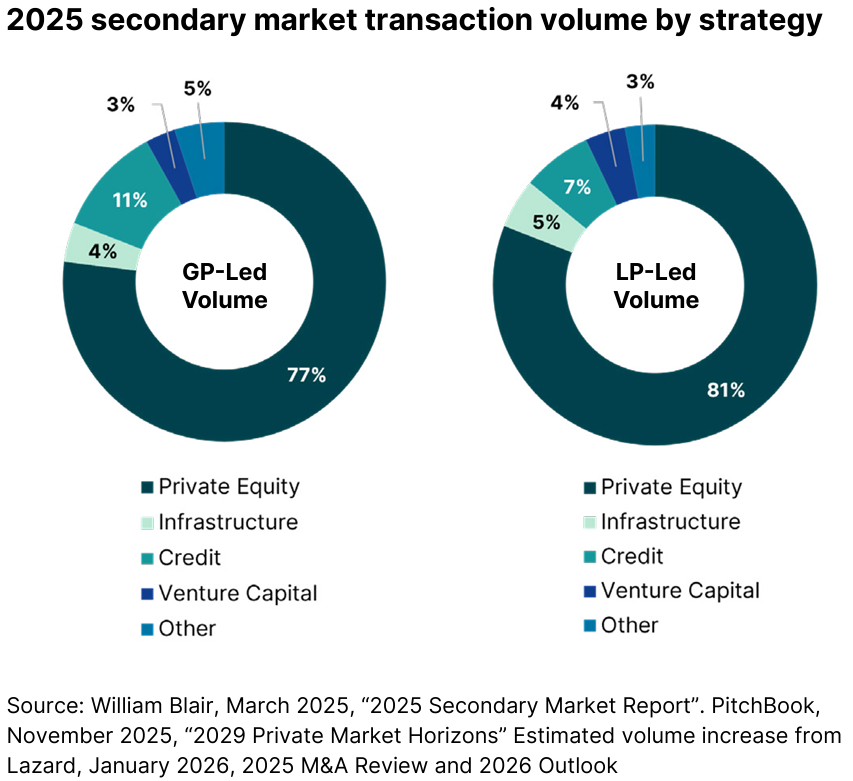

The continued liquidity challenge has driven a growing rate of activity in the secondaries market, and 2025 brought another record year for volumes.

In 2025, there were $226 billion of secondaries deals completed globally, up 41% on the previous record set the year before. Around 52% of sellers in 2025 that used the secondary market were using it for the first time, and there were record levels of sales of LP portfolios (which were up around a third year-on-year) and of GP-led deals (which rose around 50%). We firmly believe that GP-led deals are now here to stay, and at some point the volume of these transactions may surpass the sale of LP portfolios.

The current demand for liquidity will provide real investment opportunities in secondaries in the near term, although the mixed signals that continue across markets require careful navigation.