by Victor Mayer, Head of International Private Wealth | Download this article (PDF)

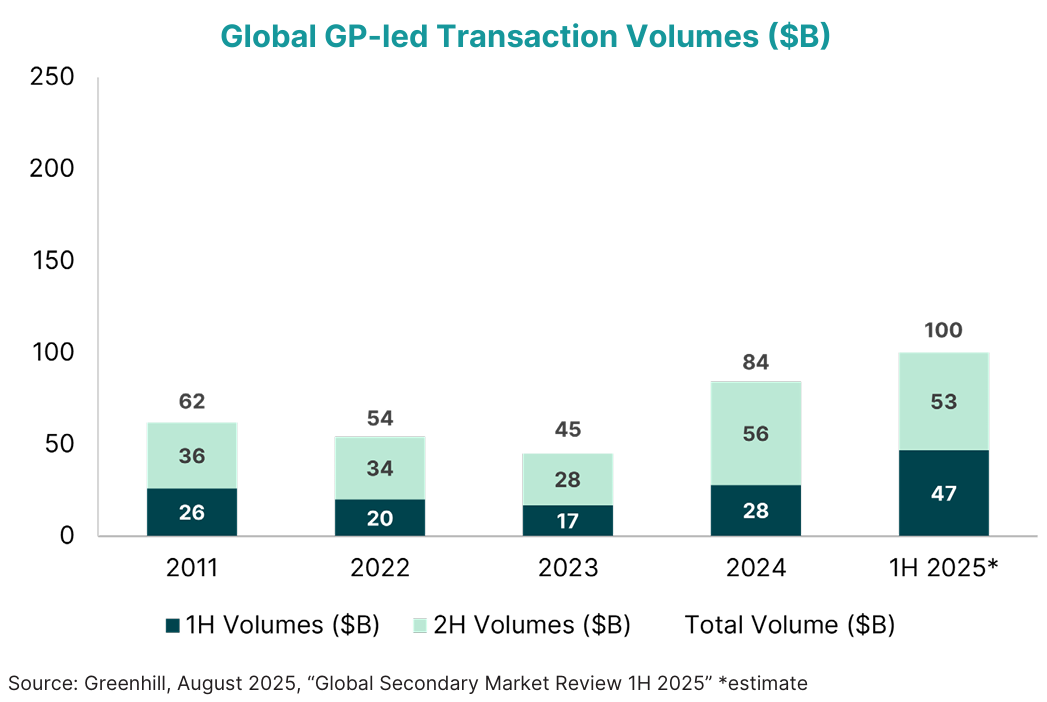

The rise of GP-led secondaries has been one of the most significant structural evolutions in private markets over the past decade. Once a niche solution for distressed or legacy assets, GP-leds have now become a mainstream portfolio management tool used by some of the world’s most respected general partners (GPs) and increasingly found in semi-liquid and evergreen strategies. And the trend has shown no sign of stopping, with the volume of GP-led deals globally reaching a new record in the first half of 2025.

In a GP-led secondary, the GP initiates a transaction to move one or more portfolio companies from an existing fund into a new vehicle (often called a continuation fund). Investors in the original fund are given a choice. They can:

- Cash out early via a secondary sale, or

- Roll their position into the new vehicle

Secondary investors can participate in these deals by buying into the continuation vehicle, often with enhanced access, improved economics, and clear visibility into the underlying assets.

““GP-leds provide investors insight into exactly what they’re investing in””

![]()

![]()

““GP-leds provide investors insight into exactly what they’re investing in””

The benefits of GP-led deals for wealth investors

For semi-liquid and evergreen platforms seeking transparency, pacing, and visibility, well-structured GP-leds can be a highly effective investment option when used selectively.

- Concentrated exposure to high conviction assets

These are not blind pools. Investors are backing known companies, often with strong performance, additional runway, and defined value-creation plans. - Visibility and underwriting clarity

GP-leds provide investors insight into exactly what they’re investing in, allowing them to perform due diligence on the assets themselves, the management teams, and the exit horizons. This can reduce blind pool and vintage risk. - Shorter duration and predictable liquidity

Most GP-leds are structured with clear exit plans over 3–5 years, making them well suited to semi liquid structures that need reliable distributions. - Economics that can have some benefits over primary commitments

Many GP-leds offer lower fees and structured carry compared to flagship fund terms. This may be particularly attractive in a net-return-conscious environment.

What to watch out for

Not all GP-leds are created equal and allocators should be aware of the potential trade-offs:

- Incentive misalignment risk

Investors need to be aware of the motivation behind a GP-led deal. Is the GP rolling the asset for long-term value creation? Or simply looking to extend fees or delay a loss? - Pricing risk

Because the GP is on both sides of the transaction (acting as both seller and buyer), conflicts can arise around valuations. While third-party fairness opinions help, pricing tension may be a point of interest. - Concentration and single-asset risk

While multi-asset GP-leds exist, many are single-asset deals. This requires strong manager conviction and diversification elsewhere in the portfolio. - Reputational filters vary

Top-tier GPs use GP-leds strategically. Others may use them defensively. It’s important for investors to discern which is which, and to participate only in well-structured, high-integrity deals. For wealth investors, due diligence isn’t just important, it’s non-negotiable.

Where GP-leds fit in a semi-liquid strategy

When used as a component of a broader multi-GP strategy (alongside LP-led secondaries and co-investments) GP-leds can offer powerful advantages:

- Accelerated deployment

- Targeted alpha

- Shorter duration

- Better pricing

“”Too many GP-led deals can reduce diversification””

![]()

![]()

“”Too many GP-led deals can reduce diversification””

However, they shouldn’t be the only secondary exposure in an investor’s portfolio. Too many GP-led deals (or the wrong kind) can reduce diversification, extend duration, and introduce unintended portfolio concentration.

Selectivity wins

GP-leds are not inherently good or bad. They are simply a tool, and as with any tool their value depends on how you use them. When used indiscriminately, or when investors rely solely on the GP’s narrative without doing their own due diligence, the strategy can fall short of expectations. But when they reflect true GP conviction, aligned incentives, and clear value-creation plans, they can deliver strong, targeted outcomes for investors.

More from our Decoding Private Markets series

Beyond IRR: Where to look for real performance in private markets

Recycling over raising: The compounding edge in evergreen and secondary funds

Understanding structures in private markets: Blending open- and closed-ended funds

Time in the market versus timing the market

Evergreen funds: a deeper look into the reasoning – and risks – of using leverage