An educational insight for private wealth investment professionals | Download this article

Pantheon believes private markets have become a core allocation for many high net-worth and ultra-high-net-worth clients. As wealth platforms continue to increase access to these strategies, a core consideration has emerged:

How should private market exposure be structured for long-term success?

For private market investors, this is no longer just a question of asset class, but of vehicle design. Understanding the differences between closed-ended and open-ended funds, and how to combine them, is essential to building flexible, resilient portfolios that align with client outcome needs.

Closed-ended versus open-ended: what’s the difference?

Private market strategies are typically accessed through two types of fund structures:

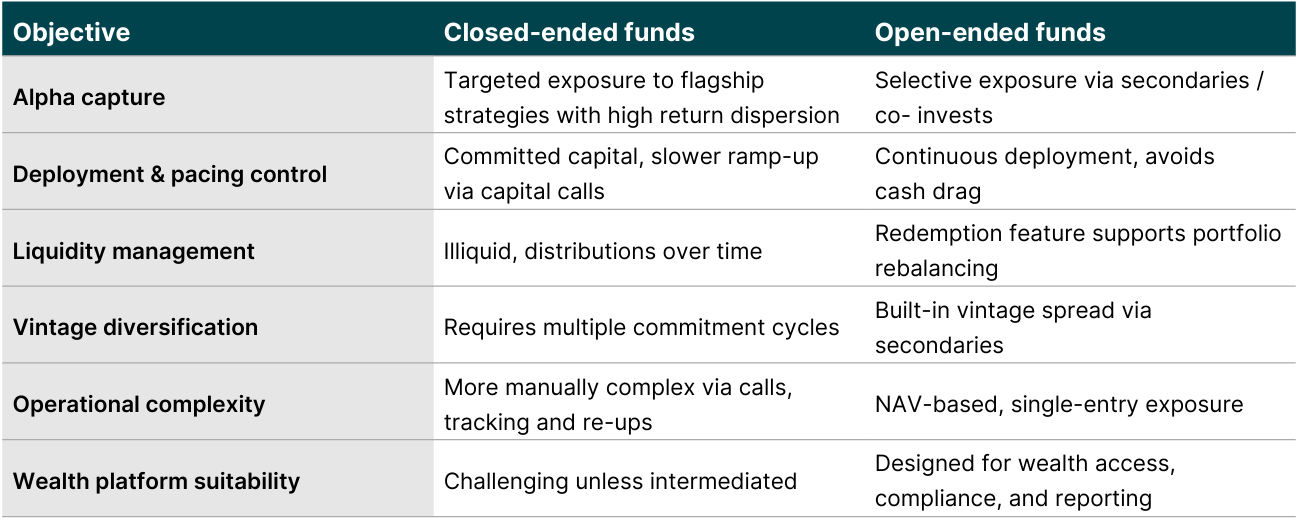

Closed-ended funds

Also called drawdown funds, these are the traditional format used by institutional investors.

- Blind pool structure, in which investors commit capital without knowing exactly how that money will be deployed. Typically have an 8-12 year life span with capital called over time.

- Capital returned through distributions after exits.

- Strategies covered include buyout, growth equity, venture capital, infrastructure, and credit.

Benefits:

- Potential access to flagship and high-performing managers and top-tier vintages.

- Structured alignment via carried interest and performance hurdles.

- Ability to target specific strategies, geographies, sectors, and pacing.

Trade-offs:

- Illiquidity, as capital is locked up and commitment-based.

- Slow to deploy, with potential J-curve effect.

- Requires managing capital calls and distributions.

- Typically higher investment minimums and more complex to access.

Typically best used for:

- High-conviction, long-term strategic allocations.

- Targeting concentrated alpha through specific vintages or sectors

Open-ended / evergreen funds

An open-ended fund and an evergreen fund both refer to perpetual investment vehicles with no set end date. They allow ongoing capital raising and periodic redemptions, unlike fixed-term funds.

While often used interchangeably, “evergreen” typically highlights the fund’s ability to recycle capital, whereas “open-ended” focuses on the continuous issuance and redemption of units based on investor activity. These funds aim to offer continuous access and periodic liquidity and are designed to be more operationally flexible.

- Structured as perpetual funds with ongoing subscriptions and redemptions.

- Assets often include secondaries, co-investments, and primaries.

- Partial liquidity available (such as via quarterly redemptions), subject to NAV-based gating.

Benefits:

- Potential for performance benefits of capital recycling and compounding.

- Simplified experience, with no capital calls and frequent top-up windows.

- Typically, faster capital deployment via secondaries and co-invests.

- Built-in vintage diversification.

Trade-offs:

- Liquidity is limited and not guaranteed.

- May have less exposure to flagship primaries.

- Potentially slightly higher management fees due to active portfolio management.

Typically best used for:

- Portfolio management and liquidity planning.

- Bridging exposure between primary fund cycles.

- Maintaining continuous private market exposure over time

Why blending both structures can work best

Each fund type offers different advantages, and used together, can potentially complement each other to help investors meet goals across liquidity, alpha generation, and operational simplicity.

A practical allocation framework

Many private market portfolios find balance by making open-ended funds the foundation and using closed-ended funds as targeted complements.

A typical allocation split could look like:

- 60–70% open-ended (evergreen / semi-liquid).

- 30–40% closed-ended (traditional drawdown funds).

The ideal blend between structures can evolve based on client goals, life stage, or liquidity needs.

Open-ended funds typically form the majority of the allocation because they are frequently the operational foundation for many private wealth investors, especially those accessing private markets through banks, platforms, or discretionary mandates. This is because of their structural advantages in smoothing cash flow management, while a NAV-based entry and exit removes the friction of capital calls and surprise distributions. Other benefits include:

- Faster deployment: potential immediate exposure via secondaries, avoiding the drag of sitting in commitment queues.

- Partial liquidity: redemptions (even if subject to limits) help match private market to private investor’s life events.

- Diversification: through secondaries and co-investments, evergreen funds may offer vintage, strategy, and manager spread without complex commitment planning.

But while open-ended funds may be ideal for the operational needs of wealth portfolios, providing solutions to issues that can frequently stop wealth investors from scaling their private market allocations, closed-ended funds can still add value. Although they often require more involvement, closed-ended funds have the benefit of:

- Capturing high-conviction investments with direct access to flagship strategies.

- Strategic exposure to niche themes and specialized sectors (such as deep tech, climate, or Asia buyout) that may not always be represented in open-ended vehicles.

- The ability to layer vintages intentionally for long-term returns.

- Stronger governance via LP rights, preferred return structures, and performance hurdles.

In a diversified wealth portfolio, closed-ended funds may serve as satellite positions offering high-impact exposures that enhance long-term return potential.

For private wealth investors, selecting the right mix of open- and closed-ended funds isn’t just an operational decision, it’s a strategic one. Open-ended funds may provide the foundation: consistent exposure, liquidity flexibility, and pacing, as well as being operationally more manageable. Closed-ended funds may add return potential and depth where it matters most.

When combined thoughtfully, they may give private wealth investors both the engine and the control to navigate private markets confidently over decades, not just cycles.

More from our Decoding Private Markets series

Why access to everything is not access to alpha

Beyond IRR: Where to look for real performance in private markets

Recycling over raising: The compounding edge in evergreen and secondary funds

Time in the market versus timing the market

Evergreen funds: a deeper look into the reasoning – and risks – of using leverage