By Victor Mayer, Head of International Private Wealth | Download this article (PDF)

The attraction of certain top-tier private equity firms is undeniable. For decades, institutional investors have leaned into the perceived safety of marquee GPs, repeating the maxim that “nobody ever got fired for investing in [insert familiar private markets brand].”

Now that same logic is making its way into the private wealth world, with an uptick in single-GP evergreen funds: closed-end structures run by one private equity house, deploying capital across its own platform and strategies.

For some, it looks like a convenient way to gain ‘one-stop’ exposure to the private markets. But what are they really offering: differentiated deal flow, or just a familiar logo?

Demand diversification

At first glance, the argument for a single-GP evergreen can seem compelling. Investors can get:

- A recognisable name

- A track record of consistent performance

- “World class” deal teams, deal flow, networks, operating value-creation teams

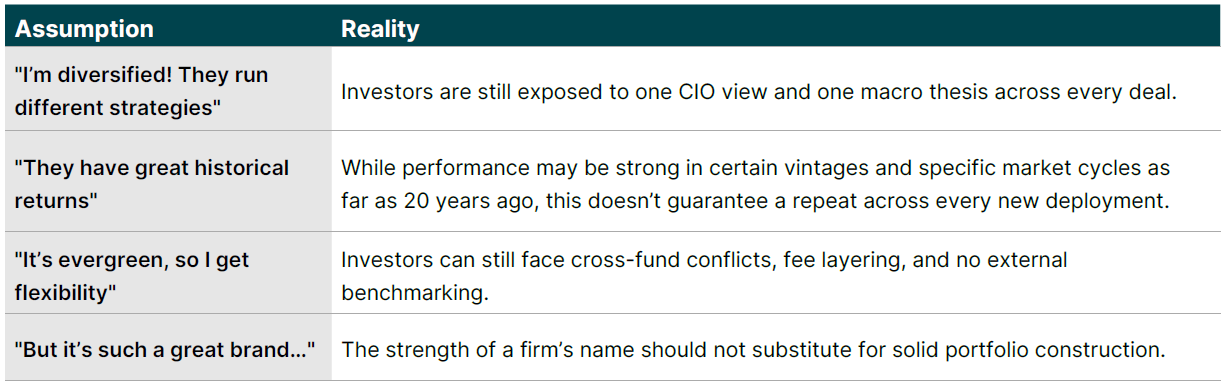

But scratch the surface, and risks emerge. These vehicles often consolidate exposure to one investment culture, one CIO lens, and one macro thesis across all sectors, geographies, and vintages. While they may offer familiarity, they can come with limited transparency, fee layering, and hard-to-navigate conflicts.

Even with the market’s most well-known names, past performance is not portable across strategies or cycles, and certainly not across every deal they do. Relying on one GP across all vintages, sectors, and economic regimes creates real structural risk.

When comfort masquerades as conviction

Investors should always ask whether their conviction in a single-GP evergreen fund is based on evidence of its thorough underwriting processes, or simply on brand familiarity and confirmation bias.

True conviction is hard-won. It requires deep diligence in a manager’s capabilities, portfolio construction discipline, and ability to navigate varying market cycles.

Too often, we see:

- Brand comfort replacing critical analysis

- Over reliance on past performance to suggest future returns

- Evergreen structure used as a ‘modern’ distribution tool

- A lack of transparency on how liquidity is managed

All of this can undermine discipline, encouraging:

- Less scrutiny of fees, conflicts, pacing, and evergreen management record

- Over-exposure to one GP’s pipeline, often across funds with a selection bias risk and with no benchmarking nor the option to reallocate dynamically

- The missed opportunity to access best-in-class managers elsewhere

What’s in a name? Assumption versus reality

The case for multi-GP evergreen: structure before style

A thoughtfully constructed evergreen vehicle can still give investors brand exposure but without brand dependence. Multi-GP structures that prioritise secondaries, co-investments, and manager selection with around an 80% allocation to these strategies, may offer:

- Access to “best-in-class” managers, not just the most well-known

- Vintage diversification across different cycles and market conditions

- High conviction investing without the single-lens blind spot

- Greater alignment through deal-by-deal underwritingand active management

- What conviction should really look like

Investors deserve more than marketing materials and a familiar name. A high-conviction private markets strategy should be manager-agnostic, actively curated, and cash-flow conscious, with continuous underwriting and monitoring. In short, it should be built for outcomes, not just optics.

More from our Decoding Private Markets series

Why access to everything is not access to alpha

Beyond IRR: Where to look for real performance in private markets

Recycling over raising: The compounding edge in evergreen and secondary funds

Understanding structures in private markets: Blending open- and closed-ended funds